This article’s title may cause some confusion. A few months ago, I wrote on quantitative tightening (QT) and, in that article, I rambled about how her big brother, quantitative easing (QE), actually works. In that rant, I stated that QE “simply accelerates existing inflationary trends that are down to strong market confidence” and does not act as a “helicopter drop.”

In the same breath, I also argued for the endogeneity of money, which sounds antithetical to the monetarist views that I had inscribed many moons ago, where I claimed that the Bank should pay attention to money growth when targeting inflation. Now, while these do seem like contradictory positions, I promise I’m not a hypocrite or, even worse, a bad writer. Economics is just pretty complex - though paradoxically, that could be because economists are quite bad at communicating - and so the goal of this article is to show that we can be pretty good at explaining things, while also absolving myself of any future accusations (hello critics!)

So let’s get into the swing of things. After a decade of low and manageable inflation, the Bank of England was caught with its pants down in the aftermath of the COVID-19 pandemic with inflation peaking at 11% back in October of 2022. This inflationary ‘hiccup,’ while still around but not as acute, has sparked fervent debate in monetary circles with two important questions. The first one is how did inflation get so damn high? The second is, is the Bank of England responsible?

To answer these questions we must first be aware that inflation management is more of an art than a science - at least in my opinion. There are many camps in the current monetary debate: monetarists, goldilocksers, wage-price spiral theorists; all propose different reasons for the current inflationary epidemic. But the truth is, all of them are kind of right. As I will show, the causes of this inflationary crisis have been a mix of money growth, cost shocks, and inflation expectations getting completely out of hand.

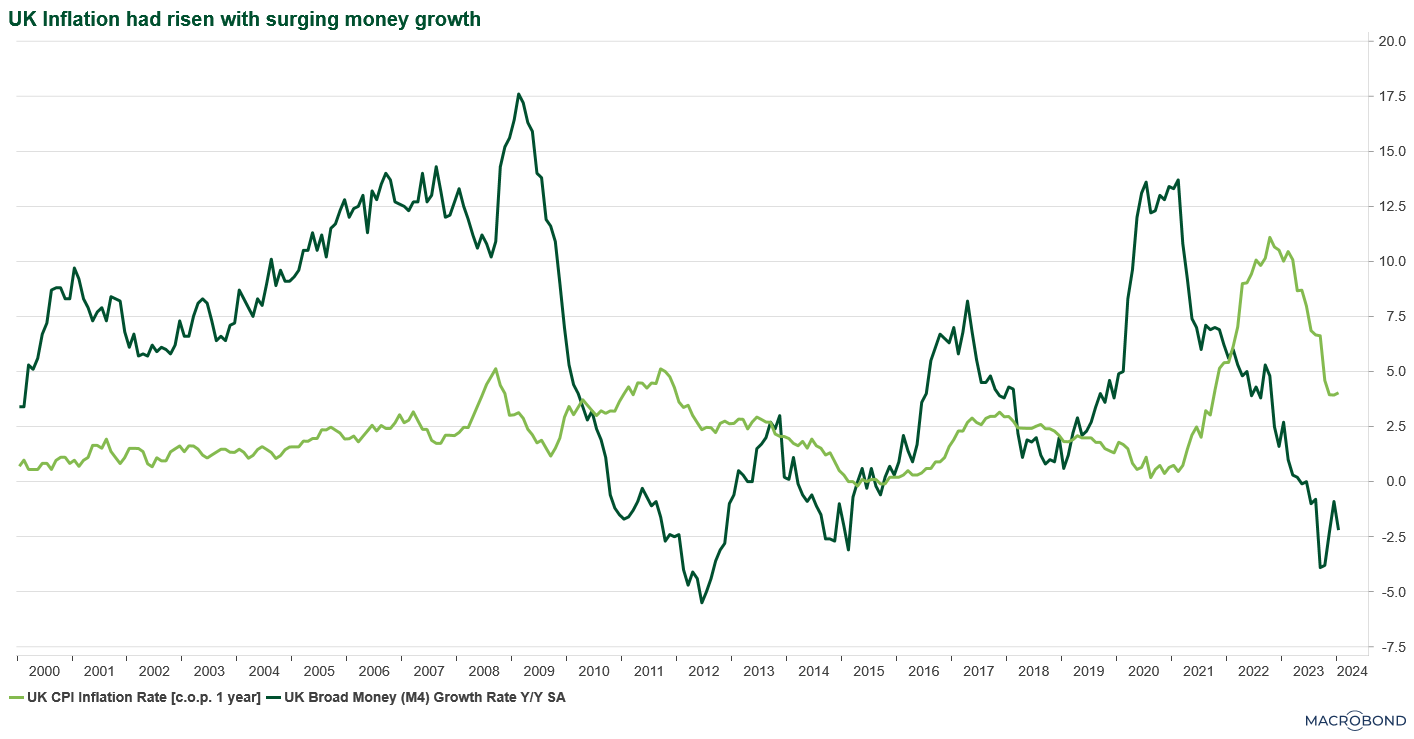

The monetarists attribute the current inflationary crisis to an explosion in broad money (measured as M4). Broad money constitutes all things that we consider money: physical cash, reserves at the Bank of England, bank deposits, bank loans, bonds and so on. Now, the monetarists are right to say that during the pandemic, the money supply did explode, and high rates of inflation followed this explosion (with a customary time lag).

However– and here comes the biggest critique– this is an inconsistent relationship. As seen in 2008 - 2009, broad money growth did explode but was not followed by high rates of inflation. So, is monetarism wrong? Not quite, but it certainly isn’t perfect.

Historically, monetarism has assumed that money is ‘exogenous.’ Effectively, this assumes the government has direct control over the money supply in the economy. This is an incorrect assumption. Going back to basics, banks ‘create’ money when they make a loan and banks only make loans when there are profits to be made. For this to happen, there need to be customers who want said loans. As such, the supply of money is not dependent on the government - or QE for that matter - it instead depends on the demand for money, which relies on factors like how healthy the economy is, customers' credit ratings, and so on. If for some reason you’d want to sound like an economist, you would say money is now seen as ‘endogenous.’

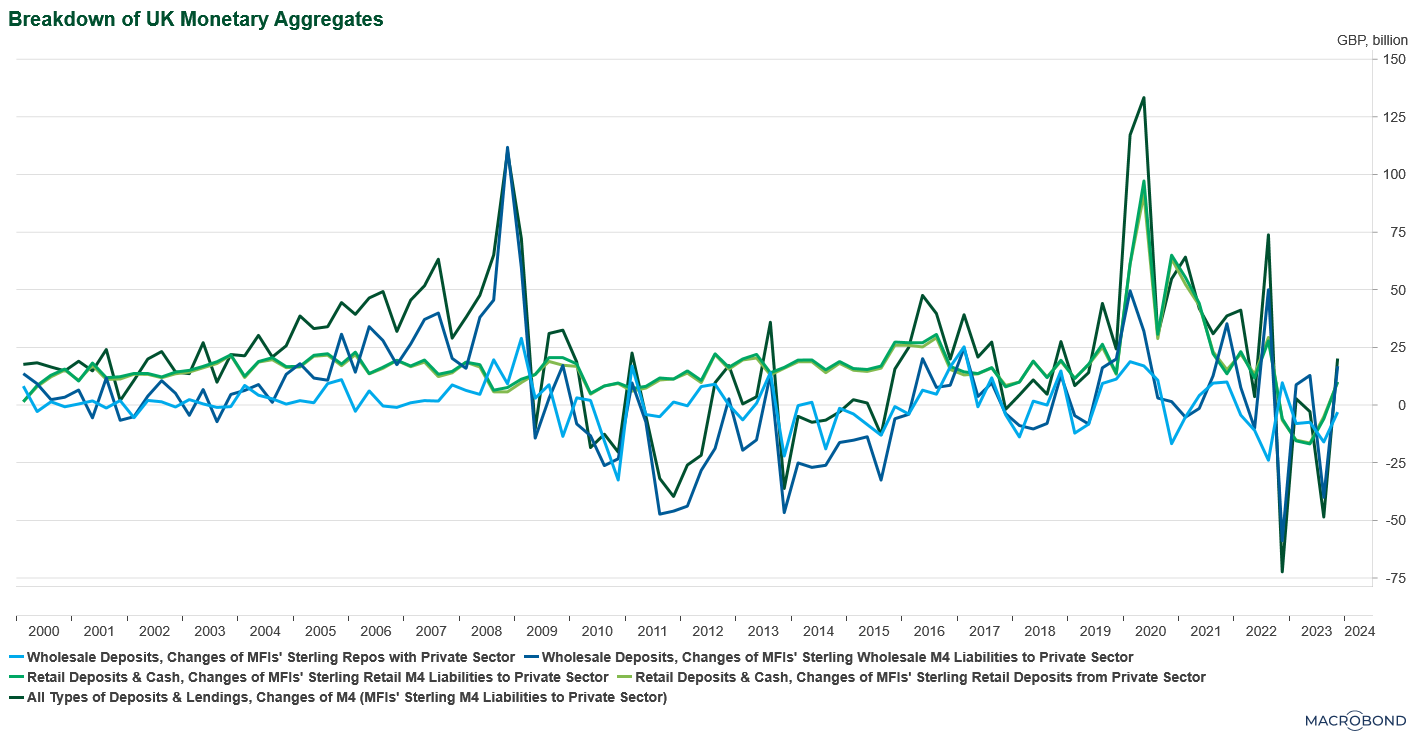

The fact that banks create money this way does not completely invalidate the monetarist perspective. As I have written elsewhere, money creation by the central bank through quantitative easing does expand the money supply, but only by increasing the demand for money itself. Understanding this gives us a direct explanation for the differences in inflationary outcomes between the global financial crisis and the pandemic. Put simply, after the financial crisis, given the lack of government support for households, workers, and businesses, money demand stayed low and inflation struggled to pick up. Instead, the huge increase in money growth occurred due to interbank lending to keep balance sheets healthy, which is denoted as wholesale assets and liabilities below:

Unlike the GFC, COVID QE was paired with the largest fiscal stimulus we have ever seen, and money demand quickly picked up after the pandemic. Thus, the majority of the ‘QE money’ manifested itself in the form of retail assets and liabilities, which represent lending to households as well as businesses, with total repo lending of QE banks being 33.6% higher than that of non-QE banks. To that end, economists have found that QE has had inflationary effects two to four times larger than those of conventional monetary measures. Such ignorance of money growth, when paired with fiscal stimulus, explains a portion of the inflationary surge. Without acknowledging this, central bank forecasting errors are sure to rise.

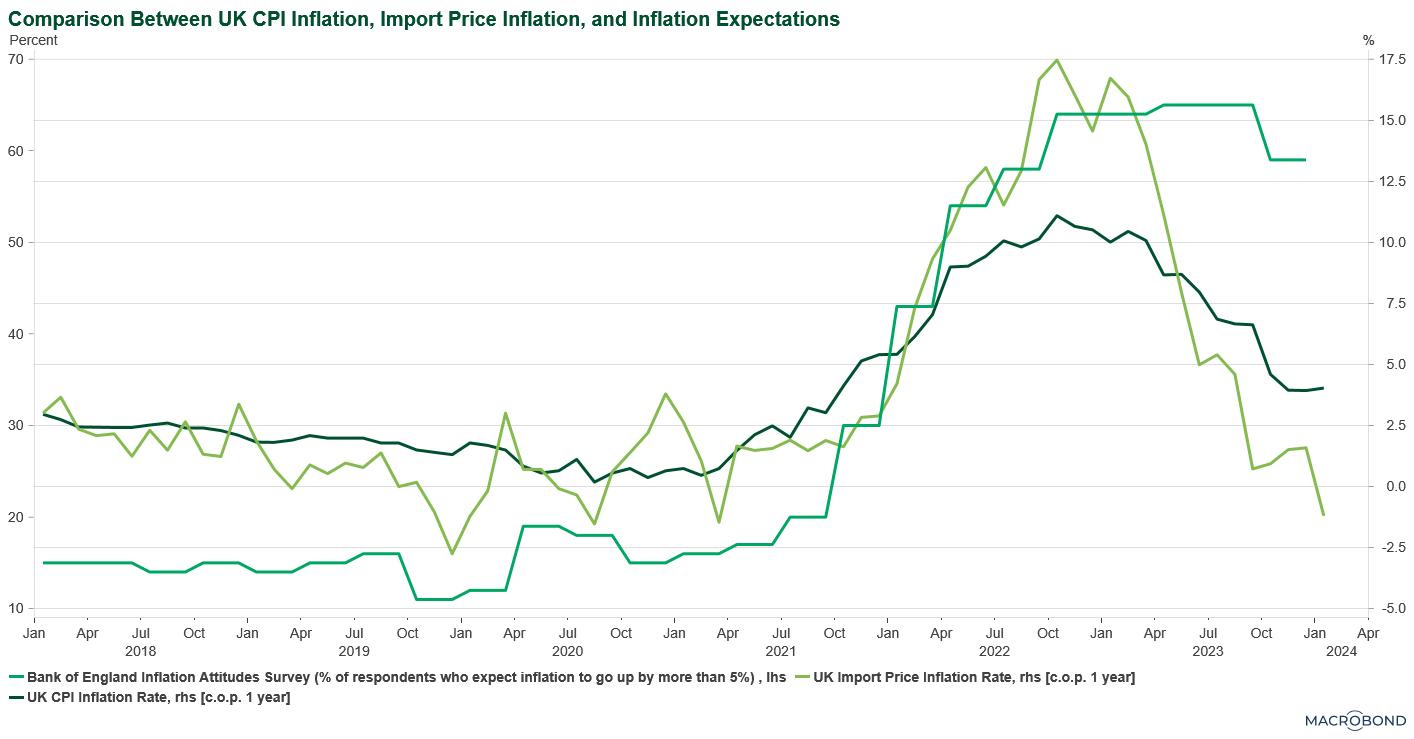

The problem herein lies in the fact that these inflationary effects of QE are exacerbated when inflation is already high. Looking at the chart below, we can see that even before the January 2021 and onwards cost-shock, measured by UK import price inflation, CPI inflation began picking up in October of 2021 as excess demand paired with supply shocks increased inflation.

From here, an unfortunate relationship occurs. As inflation rates reach between 6 - 8%, workers no longer suffer from money illusions, and start paying a lot more attention to their wages. Here, we see a wage-price spiral - where higher prices feed into higher wages. Unfortunately, central bankers failed to predict this as pre-pandemic inflation was low and stable, with workers simply not asking for drastic pay rises. Because of this, policymakers expected inflation to be transitory. This was what the wage-price spiral theorists, as well as goldilocksers, claimed went wrong.

This is the grave mistake that the Bank of England is responsible for. Yes, while central bankers cannot offset cost shocks themselves, cost shocks do bring second-round effects which ‘bake’ inflation into the economy when they are underpinned by workers asking for drastic pay rises. In our recent report, we show that had the Bank realised this, they would have imposed contractionary monetary measures a whole 6 months earlier.

Had the Bank heeded the monetarists and paid more attention to money growth, tight monetary policy would have been introduced much earlier and inflation would have been materially lower. Inflation is, of course, multifaceted and understanding it should be seen as more of an art than a science, but the Bank of England still remains partly responsible for the inflationary epidemic.